Investment Guide for Washington State Workers in PERS 2

What Do I Do With My Money? A Guide for Washington State employees already in PERS 2

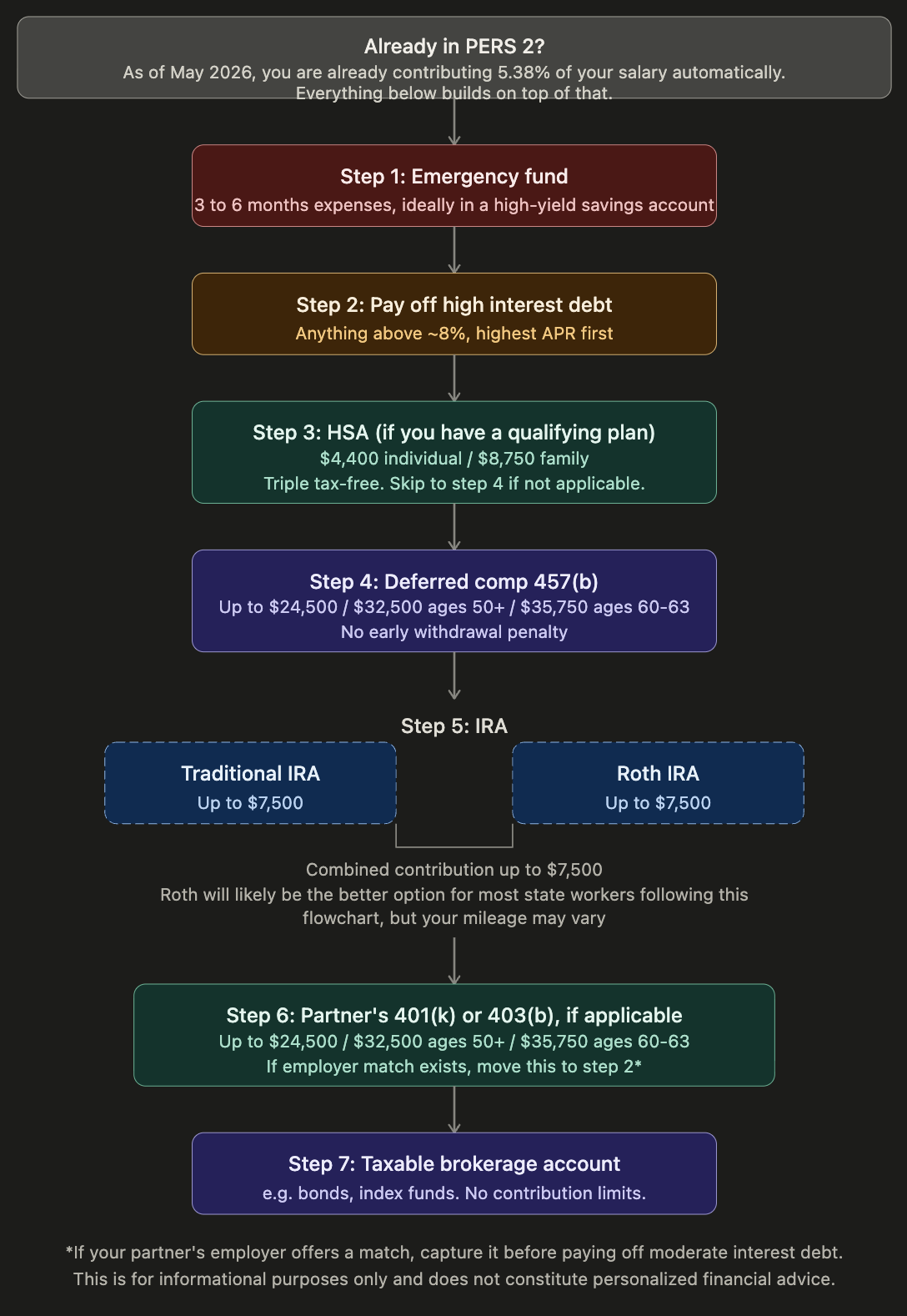

Tl;dr: The short version

Emergency fund: 3 to 6 months of expenses in a high-yield savings account

High interest debt: pay off anything above ~6-8% (depends on your goals), credit cards first

HSA: max it if you have a qualifying plan ($4,400 individual / $8,750 family)

Deferred comp 457(b): work toward maxing it ($24,500, more if you are 50 or older)

IRA: $7,500 per person, Roth may be the better fit for most state workers on this path but it will depend

Partner's 401(k) or 403(b): max it ($24,500)

Taxable brokerage: broad index funds, no limits

Long Version

This is the question almost everyone asks eventually. You get a raise, pay off a loan, or just realize you have money sitting in a checking account doing nothing. The steps below are meant to give you a clear, prioritized order for what to do with it, written specifically for Washington state workers in PERS 2. PERS 3 workers are similar and will be addressed in a different post.

One thing to note before we start: as of May 2026, if you are in PERS 2, you are already contributing 5.38% of your salary automatically every paycheck toward a defined benefit pension. That is real retirement saving happening in the background whether you think about it or not. Everything below builds on top of that foundation.

Step 1: Build your emergency fund

Before anything else, you need 3 to 6 months of living expenses sitting in a high-yield savings account you do not touch unless something unexpected happens. A car repair, a medical bill, a job gap. This is not an investment. It is protection against having to go into debt or pull from your retirement accounts when life happens.

If you do not have this yet, this is your entire financial focus until you do. Everything else waits.

What counts as a good emergency fund account? A high-yield savings account at an online bank earning 4-5% is fine. It should be accessible within a day or two but not so easy to access that you dip into it for non-emergencies. Ally, Marcus, and Fidelity Cash Management are commonly used options.

Step 2: Pay off high interest debt

Once your emergency fund is in place, tackle any high interest debt. Generally anything above 8% interest should be paid off before you do much else.

Credit cards at 20% or higher should be gone before you invest a single dollar beyond your emergency fund. Paying off a 20% credit card is a guaranteed 20% return. No investment reliably beats that.

For debt below 8%, the math gets less clear and more personal. A mortgage at 4% probably is not worth aggressively paying down when the long-term return from contributing to your deferred comp account is likely to come out ahead over time. But if carrying debt affects your stress level and your decision making, there is real value in paying it off faster even if the numbers do not perfectly support it. Use 8% as a guideline, not a rule.

A note on home mortgages specifically: if you have a mortgage on your primary residence, there are a lot of factors at play when deciding whether to pay it off early. There can be real advantages to entering retirement without a mortgage payment, for example. However, if you still have many years of work ahead, most people in the 22% or 24% federal tax bracket tend to consider making extra mortgage payments once their rate climbs above 6-8%. Below that, contributing to your deferred comp account often makes more sense from a numbers standpoint. This can be as much a personal decision as a financial one and like many situations, there may be no right or wrong answer.

How to pay off debt: pay minimums on everything first, then put every extra dollar toward the highest interest rate debt first. This is called the avalanche method and it is the approach that costs you the least in total interest over time.

Step 3: HSA, if you have one

If you are enrolled in a qualifying high deductible health plan through PEBB or your employer, you have access to a Health Savings Account. If you are not on a qualifying plan, skip to Step 4.

If you do have access to one, the HSA is arguably the single most tax-efficient account available to any American worker and most people either underuse it or ignore it entirely.

Here is why it stands out: contributions go in before taxes, the money grows tax-free, and withdrawals are tax-free as long as you spend them on qualifying medical expenses. That is triple tax-free. A 401(k) or deferred comp account gives you two of those three. The HSA gives you all three.

The 2026 contribution limit is $4,400 for individuals and $8,750 for families.

The practical argument for maxing it every year is straightforward. Unless you are planning to never have a medical expense for the rest of your life, you will eventually spend this money on something the IRS considers a qualifying expense. Prescriptions, dental work, vision, hospital bills, therapy, all covered. After age 65 you can withdraw for any purpose at all, functioning the same as a traditional IRA but with the added medical benefit throughout your life.

I will be writing a dedicated article on how to use your HSA as a retirement account, because there is a strategy here most people never learn about. Stay tuned.

Step 4: Deferred comp (457(b)), work toward maxing it

This is the account most Washington state workers are underleveraging, and it is one of the best retirement tools available to any worker in the country.

Contributions come directly out of your paycheck before federal taxes are calculated. Many state workers are in the 22% federal tax bracket. What that means in practice: for every $1,000 you contribute to your deferred comp account, your paycheck only goes down by about $780. The other $220 is money you just saved in taxes. For the privilege of investing in your own retirement, you actually pay less in taxes right now. And yes, it is completely legal.

The 2026 contribution limits are:

Standard limit: $24,500

Age 50 and older catch-up: $32,500 total ($24,500 plus $8,000)

Age 60 to 63 super catch-up: $35,750 total ($24,500 plus $11,250)

Here is a real example of what that means. Say you are 52 years old, married filing jointly, squarely in the 22% federal tax bracket (which in 2026 covers household income between $100,801 and $211,400 after the standard deduction of $32,200), and you max out your deferred comp at $32,500. By doing so, you reduce your taxable income by $32,500 and save $7,150 in federal taxes that year.

Unlike us schmucks in the private sector with our 401(k)’s, there is no 10% early withdrawal penalty on a 457(b) deferred comp account. If you leave state employment at any age, your deferred comp is accessible without penalty. For anyone thinking about retiring before 60, this is a significant advantage.

Washington State's deferred comp plan is administered by DRS. You can enroll online in about 10 minutes and start with as little as $30 per paycheck. Most people start at a modest contribution and increase by 1 or 2 percent per year, especially after a raise or when a big expense like childcare ends. The goal is to work toward the max over time. Starting is what matters.

Step 5: IRA

Once you are contributing meaningfully to your deferred comp, the next stop is contributing to an IRA. There are two types, Traditional and Roth. Which one makes more sense for your situation is a topic worth its own article, but for most state workers following this flowchart, a Roth IRA will probably make more sense. Because you are already lowering your taxable income through deferred comp contributions, paying taxes now on your IRA contributions at a potentially lower rate and letting the money grow completely tax-free is a trade that tends to work in your favor over time.

The 2026 IRA contribution limit is $7,500 per person, or $15,000 for a couple.

Income limits apply to Roth IRA contributions. For married couples filing jointly in 2026, the ability to contribute phases out between $242,000 and $252,000 of Modified Adjusted Gross Income (MAGI). Above $252,000 you cannot contribute directly.

Here is something worth understanding though. If you are a state worker who is maxing or near-maxing your deferred comp, your MAGI is already meaningfully reduced. A household earning $150,000 combined that contributes $24,500 to deferred comp and $24,500 to a partner's 401(k), and takes the $32,200 standard deduction, is looking at a MAGI closer to $68,800. The income limit is not a practical concern for most state worker households who are using their deferred comp well. Additionally, if you’ve maxed out your deferred comp, you may no longer be in the 22% or 24% tax bracket. You might have brought yourself down to the 12% tax bracket, which limits the tax advantages of a Traditional IRA.

Where to open one: Fidelity, Vanguard, and Schwab are the most commonly used providers for individual retirement accounts. Most research on long-term investing outcomes suggests that low-cost, broadly diversified index funds tend to outperform actively managed funds over time, largely because of lower fees compounding over decades. An expense ratio below 0.10% is worth looking for. Beyond that, setting up automatic monthly contributions and leaving the account alone tends to be what the research supports.

Step 6: Your partner's 401(k) or 403(b)

If your partner works for a private employer or a nonprofit and has access to a 401(k) or 403(b), that account is next. The 2026 limits are the same as deferred comp: $24,500 standard, $32,500 at age 50 or older, $35,750 for the age 60 to 63 super catch-up.

One important note: if their employer offers a match (usually something like 50% up to 4%, etc.), that match should be captured even before paying off moderate interest debt (step 2). It’s that important. Free employer contributions are an immediate guaranteed return on your money (usually 50% or 100% - unbeatable ROI). If that step was skipped earlier, go back and do it now.

Step 7: Taxable brokerage account

If you have worked through every step above and still have money to invest, congrats you are likely one of the higher paid state workers in Washington or have a wealthy spouse covering all your expenses (a very effective retirement strategy).

A taxable brokerage account is the natural next destination.

There are no contribution limits and no special tax advantages, but the money is fully accessible at any time without penalty or restriction. Most research points in the same direction as the IRA step: low-cost, broadly diversified index funds with minimal fees tend to be what long-term evidence supports.

This account is also particularly useful as a financial bridge if you are planning to retire before 59.5 and need accessible assets before your deferred comp and other retirement accounts are fully in play.

Conclusion

First, I’d like to acknowledge that most state workers will not be able to do all 7 steps. To do so would require you to invest $36,400 (maxing HSA, 457b, and IRA), on top of the 5.38% taken out for being in PERS 2. If you can do all that, amazing. If not, that is completely okay. Between your PERS 2 pension, an HSA, and any amount of deferred comp contributions, you are already doing more than most people ever will. Do not let the feeling that you can’t do it all stop you from starting.

Second, your goals may also change the order that makes sense for you. Some people cannot sleep with debt hanging over them and pay off their home before investing beyond the basics. While it might not be the most efficient wealth or tax strategy, you can’t put a price on sleeping well at night. This is meant to be a framework, not a rulebook, and hopefully it helps you feel more in control of where your money is going.

Third, remember, PERS 2 is already running in the background due to you contributing 5.38% of your salary. Everything on this list builds on top of that. I will be working on an article regarding the shockingly easy math behind retiring early as a state worker and linking back to this article once complete so you can see just how big of an impact that makes.

If you think I have something wrong, have a question, or want to share anything else, I would love to hear from you!